Personal Finance Ecosystem — India

Research Backdrop

ClearTax’s consumer business vertical includes multiple product offerings: The now-ubiquitous tax filing platform, the Chartered accountant assistance platform, and ClearTax Invest, the mutual fund product.

With a vision to simplify the layered behemoth that is consumer personal finance, we decided first to understand the complexities and nuances of the same. We planned to conduct thorough research on both users and the market to go about this. The user research would give us first-hand insights into how people approached their finances, making financial decisions, and which aspects influenced their financial behavior the most. On the other hand, the market research would give us existing solutions in the market, their positioning, and how they map to the user needs that we found in the user research.

The two lines of research were conducted in parallel and were to run independently of each other to ensure no bias. The idea was to use both lines of research as counter validations to each other. If a substantial overlap in user needs and market white space presented itself, this would essentially translate to a viable product space to take a calculated bet on. The outcomes of both lines of research would then be distilled into a user and market-validated road map for Cleartax’s consumer vertical, which aligns with the organization’s philosophy of working backward from the user to identify their needs.

The focus of this case study will be limited to user research and behavioral insight half. This case study has excluded market research, competitor research, and go-to-market strategy due to IP and NDA purposes.

Research Aim

Personal finance can be broadly divided into Income, savings, spending, assets, investments, liabilities, and misc. The research aimed to understand different types of consumer behavior w.r.t the aspects mentioned earlier of one’s financial life and identify patterns of behaviors. We also tried to understand users’ motivations behind such behavior and the pain points that led to such unique behavioral patterns. Another important point of inquiry was the triggers that influenced the aforementioned financial decisions and behaviors the most.

User Sourcing

ClearTax’s Tax filing tool is one of the most ubiquitous tools in the national financial landscape. Many consumers use it for the seamless filing of their taxes. The NPS of the tool is relatively high, and that gave us a channel we could harness qualitative user feedback from.

While conducting feedback sessions for the filing tool, we floated an optional opt-in for an additional user research session about personal finance and investment methods/patterns. A simple reward system of coupons was set up for the participants. Hundreds of users voluntarily opted in for the research sessions, and we scheduled one-hour call sessions with each user, thanks to Calendly.

Research Questionnaire

To understand users’ financial decisions and the stories behind them, we framed a questionnaire that built inquiry from the existing financial footprint of a user.

As mentioned earlier, the questionnaire would probe multiple aspects of a user’s financial journey:

- Life goals

- Income data

- Spend pattern

- Savings

- Asset pattern

- Investments

- Liabilities

- Insurance and securities

- Others

The line of inquiry started with specifics and facts that users already knew about themselves and experienced daily before ultimately diving into their personal lives and getting them to vocalize longer-term goals that people seldom vocalize on their own. The aim was to build rapport with the user through facts and stories to make them comfortable enough to share personal and usually ambiguous motivations.

Each question started on its own as an open-ended question that probed a user on a specific part of their financial journey. A set of more specific questions were put in place, which was deployed after specific pre-set, triggers corresponding to them were met. This allowed interviewers to catch users at the right points and probe on specifics or reasoning behind certain behaviors.

Users were also primed before we got into each category. The minimal requisite terminology was explained to users with examples before the research team raised the actual questions. This also helped us build some rapport with a user before we let the user do the talking. This eased the user into the conversation and helped us get more qualitative insights.

Here is an example from one of the users in the pilot study:

Interviewer: Do you invest money? Investing money is putting money in things like Fixed deposits, savings accounts, stocks, mutual funds, PPF, EPF and other instruments like that. It is mostly money meant for future use; money that you think will grow.

User: Yes.

Interviewer: Great! across what instruments out of the ones I told you before do you invest?

User: I have some money in my savings bank account and some in a fixed deposit. Have a PF account with my bank as well.

Interviewer: Why did you decide to invest in these particular instruments and not the other ones?

User: Because there is no loss in these. I invested in mutual funds at one time. But I got some losses. And I am not in a position to take such risks with my family. So, stuck to savings bank and fixed deposits.

Interviewer: Do you intend on trying any other investment instruments in the future?

User: There are some schemes from LIC which are interesting. Will probably consider those. Wont invest in stocks and all. Those are akin to gambling.

Interviewer: Why are you considering these schemes?

User: A friend has invested in them he says there are good returns with minimal risk. Seems like a good bet.

In the above conversation, factoring in the income, spending, and liability data, one can get a much clearer picture of financial behavior and the reasons for such behavior.

We then headed to pilot this interview with five users.

Pilot Study

In the pilot study, we faced a couple of issues, which we had to workaround.

1. Users were reluctant to share their financial details.

Inhibitions to sharing such closely guarded data are only natural. Hence, there was a need to put users at ease, much more so than usual.

First came a section of introductory notes for the interviewer to present to the interviewee. These notes primed a user about the aims and function of user research and how a user’s data would be utilized after collection. This was essential to create a sense of security and ease user inhibitions about divulging financial data, which is closely guarded and rarely revealed.

Post the primer, the interviewer would then give the interviewee a brief history of themselves, followed by a picture of their finances. This immensely helped bring the walls down with the users, and they readily shared their rationale behind their investment decisions.

2. Users did not like sharing numbers.

There was a two-pronged approach to solving this problem:

- Before each question was asked, we included a brief section where the interviewer would reveal their financial picture about that section with numbers. We noticed that this significantly increased the probability of users sharing numbers. Here is a rough sketch of the note.

Interviewer: (If the user answers “Yes” if he / she has investments in equity): Ah, Nice! Even I invest in shares and mutual funds. Recently, as you might have noticed, the market had a major upturn. Ever since the announcement made by the finance minister in the latest Union budget. I immediately invested a sum of 50,000 in stocks and 20,000 in mutual funds.

User: Ah, yes! I missed that opportunity. I have some 30,000 invested as well. Maybe I will invest further after there is a dip in the markets.

2. If the user was still reluctant to share details of numbers with us, we went ahead and equated them on a scale of 10. Further, we changed the income level to brackets, which the users were much more likely to share. Here, the conversation changed to:

Interviewer: What would you say is your rough annual income bracket from all income sources? The brackets are:

Below 5 lakhs, 5–10 lakhs, 10–20 lakhs, 20–30 lakhs, 30–50 lakhs, 50 and above

User: 5–10 lakhs

Interviewer: If your total income was 100 rupees, how much out of it would you say you save, spend or invest? For example, I spend 40 rupees, save 20 rupees and invest the other 40 rupees.

User: I think I spend 60, save 20 and invest 20

Interviewer: Great. Let’s talk about where all you invest. FDs, Stocks, mutual funds, PPF?

User: I have some FDs and then there’s some mutual funds

Interviewer. Now, out of the 20 rupees you invest, what would you say is the split between FDs and Mutual funds?

User: I think 15 rupees in FDs and 5 rupees in mutual funds

3. Users readily shared details of good investments. Did not readily share bad investments.

Again, after noticing this, we included stories of the interviewer’s own bad experiences with investing in equity-based markets. This helped the users open up about their own bad experiences.

After learning that the user invests in equity-based markets...

Interviewer: That’s nice. I’ve also invested a lot into shares last year. Around 60,000 I think. But because of the market falling down, I lost around 20,000 out of that. Post that, I decided to take out some 20,000 and let the other 20,000 remain. I hope you have had better luck with these things?

User: Yes. even I have faced major losses. I think I lost around 50,000 this year when the whole motor segment crashed down. But I am hoping they will pick up again due to the electric vehicles coming into the market. So, I have not pulled out my money yet.

Interviewer: That’s interesting. You must have invested much more than me, in that case.

User: Yes. I invested around 2 lakhs.

4. Users started asking us for financial advice.

For this part, we promptly denied offering any advice to the user to maintain our neutrality. We advised users to approach a professional CA to plan their finances and offered to refer them to the ClearTax group of CAs if required, to which many users readily agreed.

5. Financial Bias due to Life goals

We initially started each user session with a summary of their life goals. What we observed in this pattern was that users tried to alter the narrative of their finances to fit their life goals. Many users seemed to realize that their life goals and finances were disconnected and tried to find links between them.

The solution to this was simple. In the revamped questionnaire post the pilot study, we moved the section on life goal inquiry right at the end; after eliciting all financial data. This helped us cut the unnecessary context and caught the users unaware and unbiased. This ensured we got a clear picture of both; the customer's finances and the life goals.

6. Vocalising secondary life goals

Further, many users had a problem vocalizing their life goals. Many married people stopped with their life goals of being limited to their children’s education and house loan repayment / owning a home.

For this portion, too, we added some example goals through the interviewer before the user opened up. This helped the user realize and vocalize their own goals that have been slightly deprioritized for public reception.

(After the primary goals were mentioned)

Interviewer: That’s great. Do you have any other kinds of goals that you really want to achieve, but have not made much progress on? Like for example, I have wanted to do a euro trip in a long time and also wanted to start a farm of my own. But I am so lazy, I have never made any progress on both of them. Is there anything that fits that kind of profile for you?

User: Umm, yes. I think even I have wanted to travel with my family for a long time. We wanted to go to Kashmir. But I am having to put that off for a while now. I think I should do something about it.

Also, maybe I wanted to start a business of my own. I wanted to set up a bakery for my wife. I think I have to slightly look at that too.

7. Language

In the pilot tests, we observed that using a person's mother tongue instead of using English as a medium helped users ease into the interview. It also helped break the ice faster and generate more trust. A small 2-minute small talk at the beginning of the discussion in the user's mother tongue helped a lot in breaking the invisible walls.

We then made a team of 8 people who could speak different languages among ourselves. These languages included: English, Hindi, Tamil, Telugu, Kannada, Bengali, Marathi, and Malayalam. We paired each user with an interviewer who could speak their mother tongue, captured in the interview opt-in form. For some users whom we had already captured details about, we dropped a text to get this crucial information point.

Interviews

Most interviews happened on phone calls as the users of the interview were spread across the country. We actively opted for voice calls over video calls as these sometimes tended to induce anxiety in the customer.

We made a google form where we could capture all the data we needed. Each interviewer had a partner who would focus on the data entry while the interviewer interviewed the user on speaker. The audio call also helped with this aspect of the interview, masking the data capturer to the user, which otherwise would have induced more unnecessary anxiety and nervousness in the user.

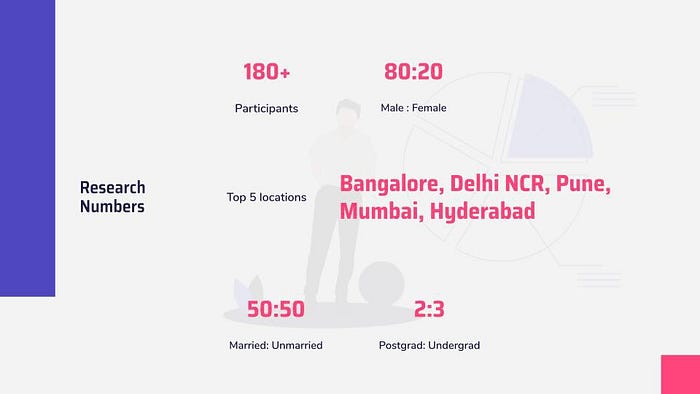

The Numbers

Affinity Analysis

At the end of each day, all the interviewing teams (5 teams, ten people) caught up and exchanged key qualitative stories encountered in the user sessions. After completing all the interviews, which took around 2.5–3 weeks, we deconstructed the google sheet that was used to collect data from the users.

We affinity mapped them and found clear patterns of user behavior w.r.t finances based on a User’s age group and income level. Age provided a more direct correlation between life goals and financial habits. We used this as a primary data point to form user buckets, analyze data, and elicit their needs.

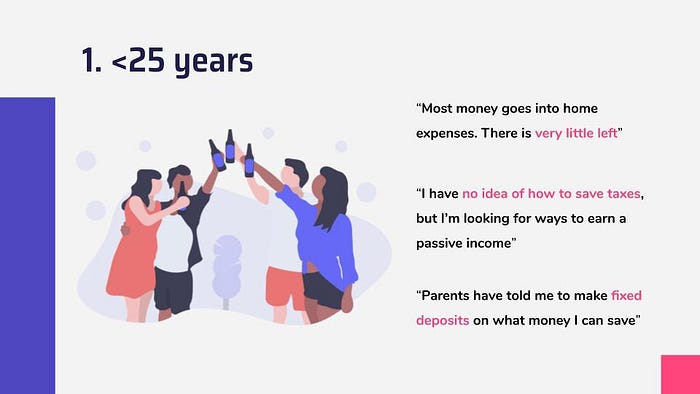

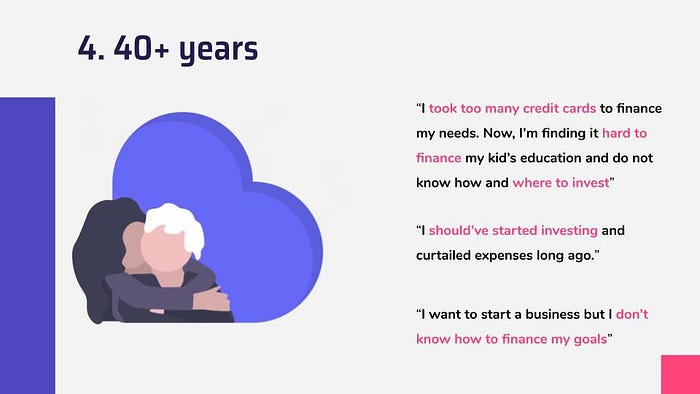

User Segments

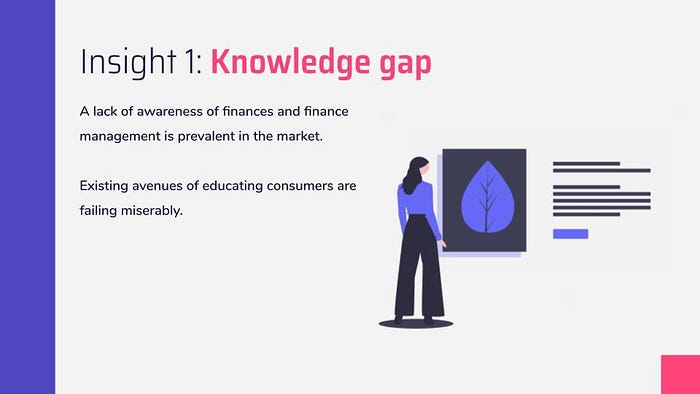

Insights

Without revealing all the deeper insights related to the study, these were some top-level insights we had. The deeper insights used for making the product roadmap and the business plan have not been revealed here.

But here are some tidbits:

Learnings

1. One size does not fit all

We initially started the research with a set questionnaire that went in a set of questions. Soon, we realized this pattern does not work across users, who vary from different ends of the financial and personality spectrum.

Instead, the questionnaire became more of a checklist of topics to discuss and get the user talking.

2. Let the user lead the conversation

Another folly of a structured questionnaire was that we initially started bombarding users with many pointed questions. This led to the users feeling like they were being interrogated for a crime. We flipped this approach around during the pilot tests and merely redirected the conversation at the right time while letting the user lead the discussion most of the time. Once users got into a free-flowing conversation with the interviewer, the real insights flowed.

3. Transparency breeds trust

As exhibited by the numerous hacks described earlier, the most important thing was to humanize the interviewer and reveal our cards first. This broke down a lot of walls with users, and most of them readily shared otherwise confidential financial data with us and provided us with many insights.

4. Ask questions that elicit stories; not data points

Another learning from the whole interviewing experience was not asking very direct questions. Instead, users naturally paved their way to the data point we needed when we asked questions that often came before the actual question. E.g., Instead of asking, “How many insurance plans do you have” a precursor to that would be: “In case something unfortunate happens to you, how will your family take care of themselves?”. From here, the users’ stories naturally included all the data points needed for us to collect. These also gave us a lot of insights that we otherwise would have missed out on.

Bonus

The highlight of the interview process was a 56-year-old man who had opted in for the interview. As soon as we talked to him for a minute, he asked us if we could give him our organization account number. When asked why he replied, “ClearTax has been helping me file taxes without any help for the last three years. You have given me an excellent service for free. I am very grateful to you. So I thought I should give you people some money to encourage you on your path. Thank you so much”.

This made our day, month, and year.

Epilogue

This research session was conducted in conjunction with Abhinav Krishna, Aditya Raghunath, Akshay Bharadwaj, Amit Srivastava, Aravind Bachu (Too many “A”s, I know), Sunny Paul and Medha Seth (phew), all beautiful people who made working in the consumer vertical at ClearTax an absolute pleasure. Shout out to you guys.

Thanks to undraw for the beautiful illustrations on the slides.